Bogus Fee Alert

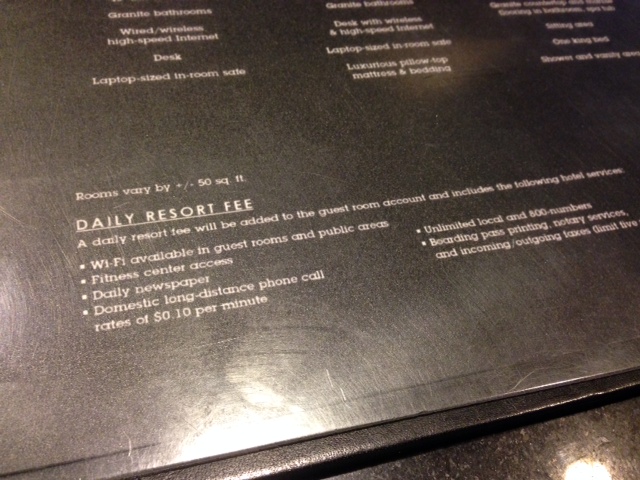

My daughters and I are in Las Vegas after a wonderful trip to 3 national parks. I bid for and prepaid for a hotel in Las Vegas, "New York, New York." Priceline told me that my "Total Price," including "Room Cost," "Taxes" and "Fees" was $80.88. When I stepped up to to register for the room. the NY NY employee told me that I owed a "Daily Resort Fee" of $24. She pointed to a pamphlet on her desk (see the attached photo) and told me that the "fee" is for these items, including "unlimited local and 800 number calls."

I told her that I already paid the "Total Price," and I would not pay this "Fee." She told me "Everyone pays this fee." I told her that I wouldn't pay this "Fee," because I already paid all "fees." She said I needed to take it up with Priceline. I told her I needed to speak with her manager. The manager (another woman) came to the front desk and told me "All of the resorts in Las Vegas charge the fee." This was no consolation to me. She told me that I had to pay the fee. She told me that Priceline discloses that I would be responsible for paying this additional fee (this is false). I told her that I wouldn't pay the fee, that it was fraud to charge the fee, and that I would pay it under protest, contesting it through my credit card company. I told her that I was a class action attorney and that they should be sued for a class action. The manager finally admitted to me that since Priceline told me that I had prepaid my "Room Cost," "Taxes" and "Fees," that it would be "unfair for me to pay an additional "fee." She wagged her finger at me and stated that she would waive the fee this time only.

I am disturbed that this is going on. I assume that hundreds or thousands of people are being hit for this "Fee," and that most of them are paying it rather than making a scene at the registration desk.

For any of my FB friends who are using Priceline to book rooms in Las Vegas (or elsewhere), beware that this is going on. In my experience as a consumer lawyer, merchants are increasingly tacking on these BS fees for illusory services, fraudulently making millions of dollars in the process.